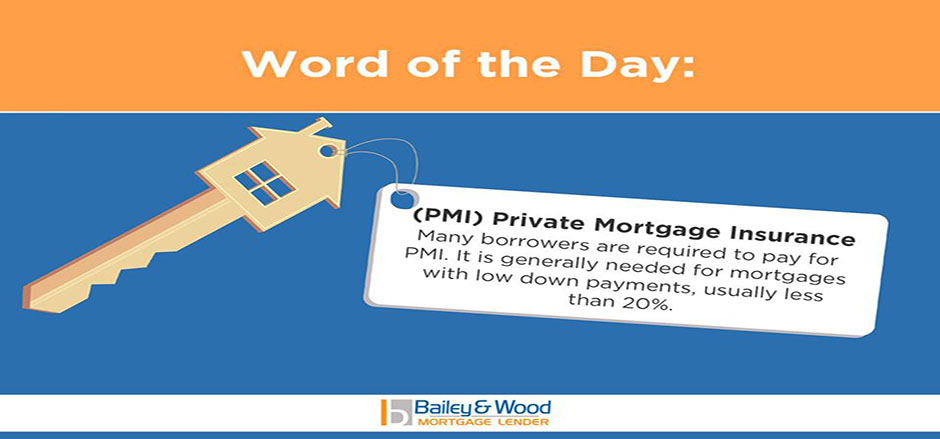

PMI is a layer of protection for lenders, but an added expense for you as a borrower. Conventional loans are the most popular type of mortgages, but they’re also the one that isn’t insured by the government.

Once you’ve paid 20 percent of your home’s loan-to-value ratio, you can contact your lender about removing PMI from your mortgage payment. Keep in mind that PMI doesn’t go away automatically; you must request it.

While PMI is required for some loan agreements, it’s not for all. Here are a few ways to avoid private mortgage insurance:

1. Put 20 percent down. The higher the down payment, the better. At least a 20 percent down payment is ideal if you have a conventional loan.

2. Consider an FHA loan. The minimum down payment for an FHA loan is 3.5 percent. This is a good option if you have less-than-stellar credit, but the closing process could take a little longer with this option, and FHA loans have higher fees.

3. Cancel PMI later. If you couldn’t get out of private mortgage insurance when you bought your home, keep track of your payments. Once the loan balance reaches 80 percent of the home’s value, you can ask the lender to drop the mortgage insurance premiums.